.avif)

%201.svg)

HIPAA Compliance Checklist for 2025

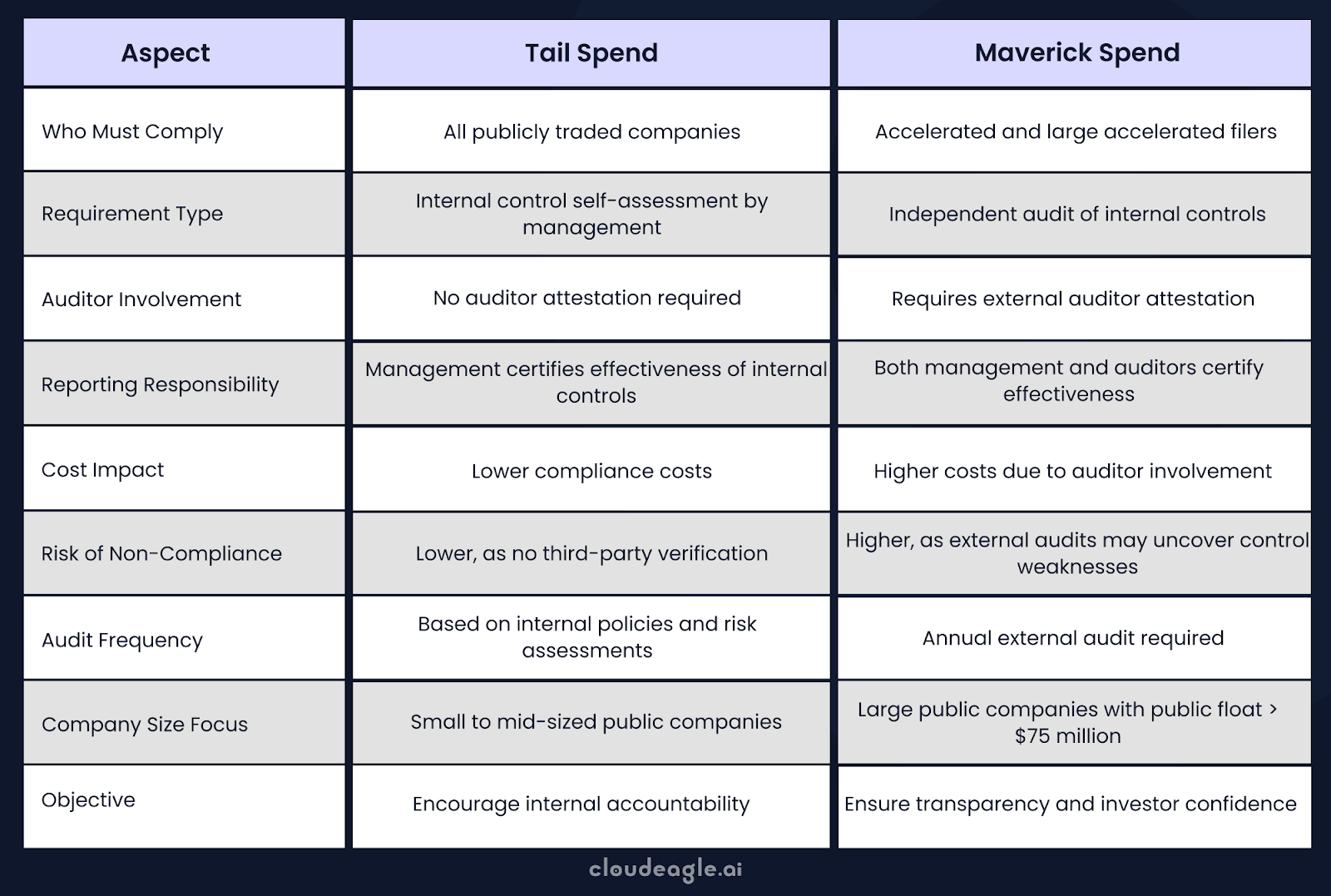

The procurement process is a key part of how companies manage their finances and controls under SOX Section 404. Understanding the difference between 404a and 404b helps businesses know what compliance steps they need to take.

Section 404a requires management to evaluate and report on internal controls, while 404b involves an independent auditor verifying that assessment.

Think SOX compliance is just a box to check? Think again. The shift from 404a to 404b isn’t just about an extra audit; it brings greater oversight, deeper financial security, and new operational demands.

Many companies underestimate the preparation required for external auditor attention, which may lead to face unexpected spending along the way.

This article breaks down SOX 404a vs 404b, clearing up the confusion on what changes, why it matters, and how to prepare without blowing your budget or overhauling your processes.

TL;DR

- SOX 404a requires companies to self-assess internal controls, while 404b mandates external auditor validation, increasing scrutiny and costs.

- Who must comply? Companies with a public float above $75M must transition from 404a to 404b, triggering higher audit fees and stricter reporting requirements.

- Why is SOX 404b expensive? Audit fees range from $500K–$1M annually, with companies seeing a 58% increase in compliance hours due to external auditor demands.

- How to control costs? Automating compliance, strengthening internal controls, and conducting mock audits can reduce audit scope and expenses.

- Avoid common pitfalls like poor documentation, reliance on manual processes, and lack of team coordination lead to audit failures and financial risks.

- CloudEagle.ai streamlines SOX compliance by automating governance, streamlining access control reviews, and ensuring audit-ready reporting with minimal manual effort.

What is SOX 404 Compliance?

SOX 404 Compliance refers to the requirements under Section 404 of the Sarbanes-Oxley Act of 2002, which mandates that publicly traded companies establish, document, test, and maintain effective internal controls over financial reporting (ICFR).

The goal is to ensure the accuracy, reliability, and transparency of financial statements, thereby reducing the risk of corporate fraud and protecting investors.

But not all companies follow the same rules. In SOX 404a vs 404b, both define two different levels of compliance. One relies on management’s word. The other? Requires an auditor’s stamp of approval.

Let’s break them down.

1. What is SOX 404a?

SOX 404a is the lighter version of compliance, applying to all public companies.

SOX 404 a requirements

It requires management to:

- Assess and document their internal controls.

- Certify that financial statements are accurate.

- Report their findings in annual filings.

No external auditor attestation is required - which means lower costs and less scrutiny. But companies must still ensure controls are effective because if investors or regulators lose trust, the consequences can be severe.

Who follows SOX 404a?

- All publicly traded companies must comply.

- Non-accelerated filers (companies with a public float below $75M) don’t need an external audit under SOX 404b.

2. What is SOX 404b?

SOX 404b raises the stakes. It requires an independent auditor to verify a company’s internal controls; no more self-assessments.

SOX 404 b requirements

Here’s what companies under 404b compliance must do:

- Hire an external auditor to test and validate their internal controls.

- Provide evidence that their controls effectively prevent errors or fraud.

- Face additional scrutiny, with auditors digging deep into processes, IT systems, and risk management.

Who must comply with SOX 404b?

- Large accelerated filers (public float of $700M+).

- Accelerated filers (public float between $75M–$700M).

Who’s exempt?

- Emerging Growth Companies (EGCs) for up to five years after their IPO.

- Non-accelerated filers (public float under $75M).

In SOX 404a vs SOX 404b, the shift from 404a to 404b isn’t just a formality; it’s a financial and operational burden if not managed properly.

SOX 404a vs 404b: Quick Comparison Table

SEC Filer Categories and Thresholds

The SEC classifies public companies into several filer categories based primarily on public float (the aggregate market value of shares held by non-affiliates) and other criteria. The main categories are:

- Large Accelerated Filer: Companies with a public float of $700 million or more.

- Accelerated Filer: Companies with a public float between $75 million and less than $700 million.

- Non-Accelerated Filer: Companies with a public float of less than $75 million or those that have not met certain reporting requirements.

- Smaller Reporting Company (SRC): Companies with a public float of less than $250 million, or with less than $700 million public float and annual revenues under $100 million.

Public float is measured as of the last business day of the company’s most recently completed second fiscal quarter (e.g., June 30 for calendar-year companies).

The thresholds for moving between categories can be lower if the company previously qualified as a certain filer type (e.g., moving from large accelerated filer to accelerated filer requires a public float below $560 million instead of $700 million).

How to Know Which Category You Fall Under?

To determine your SEC filer category:

Calculate Public Float: Multiply the number of common shares held by non-affiliates at the end of the second fiscal quarter by the closing stock price on that day.

Identify Affiliate Holdings: Exclude shares held by affiliates to ensure an accurate public float.

Compare Public Float to Thresholds: Use the thresholds for large accelerated, accelerated, non-accelerated, and smaller reporting company categories.

Consider Revenue Test for SRC: If public float is not determinative, use annual revenues (less than $100 million for SRC) as a secondary test.

Review Prior Filing Status: If the company previously qualified as a certain filer type, lower thresholds may apply for category changes.

Check Emerging Growth Company (EGC) Status: EGC status depends on factors like total gross revenues, time since IPO, debt issuance, and filer category.

By following these steps and referencing Rule 12b-2 of the Exchange Act, companies can confirm their filing status for SEC reporting and deadlines.

This classification affects important deadlines and reporting requirements, such as Form 10-K filing dates and compliance obligations.

What Is Top-Down Risk Assessment (TDRA) and Why It Matters?

Top-Down Risk Assessment (TDRA) is a structured approach used in financial auditing and internal controls, especially for compliance with Section 404 of the Sarbanes-Oxley Act (SOX 404). The TDRA method starts at the highest organizational level and systematically narrows focus to specific accounts, processes, and controls that present the most significant risks to financial reporting.

Key Features of TDRA

- Starts at the Entity Level: The assessment begins with a review of company-wide objectives and risks, such as the overall control environment and governance structures.

- Focuses on Materiality and Risk: The approach prioritizes areas that could have a material impact on financial statements, ensuring resources are directed to the highest-risk areas.

- Drills Down to Significant Accounts and Disclosures: After identifying high-level risks, TDRA narrows its focus to key accounts, transactions, and related controls that are most likely to affect financial reporting accuracy.

- Evaluates Both Entity-Level and Assertion-Level Controls: Controls are assessed at both the broad organizational level and the specific assertion level (e.g., accuracy, completeness, existence of transactions).

Why TDRA Matters for SOX Compliance

- Efficient Resource Allocation: By focusing on the most significant risks, TDRA helps organizations avoid unnecessary testing of low-risk areas, reducing compliance costs and effort.

- Enhances Effectiveness: The method ensures that critical controls over financial reporting are thoroughly evaluated, increasing the likelihood of detecting material misstatements or control deficiencies.

- Supports Regulatory Expectations: The Public Company Accounting Oversight Board (PCAOB) and the SEC recommend a top-down, risk-based approach for SOX 404 compliance, as outlined in PCAOB Auditing Standard No. 5 (AS5). This ensures that companies meet regulatory requirements and best practices.

- Facilitates Remediation: By identifying high-risk areas early, organizations can prioritize remediation efforts and address control weaknesses before they impact financial reporting.

A Smarter Way to Manage SOX Compliance

Implementing TDRA offers a smarter, risk-focused strategy for SOX compliance:

- Streamlines Testing: By concentrating on high-risk accounts and processes, companies can streamline their internal control testing and reduce redundant work.

- Improves Audit Quality: Auditors and management can better demonstrate that they have addressed the most significant risks, leading to more robust internal controls and reliable financial statements.

- Reduces Compliance Costs: Focusing on material risks and significant controls means less time and money spent on low-impact areas, making compliance more sustainable in the long term.

Enables Proactive Risk Management: TDRA encourages ongoing risk assessment and timely updates to controls as business processes and risks evolve.

The Cost and Compliance Burden of SOX 404b

The shift from SOX 404a vs 404b brings a significant financial commitment, as external audits under 404b introduce added complexity and costs. The moment a company crosses the $75M public float threshold, compliance costs skyrocket, audits become more invasive, and internal teams feel the pressure.

SOX 404a vs 404b - Why Does SOX 404b Cost More?

External audits are expensive – Unlike SOX 404a, where management assesses its own controls, 404b requires independent auditors to validate internal controls over financial reporting (ICFR).

That means higher audit fees and more billable hours from external firms. In fact, external auditors rely on only 29% of companies’ internal control testing, requiring them to perform extensive independent testing.

Stricter documentation & testing – Companies must prove their controls are effective. That means extensive documentation, additional testing, and more time spent preparing for audits instead of focusing on core business functions. 88% of companies involve their internal audit team in SOX activities, with 67% handling controls testing directly - a major internal resource drain.

More scrutiny, more risk – Regulatory bodies have increased their oversight in recent years, making it harder to pass audits without deficiencies. 75% of organizations reported control deficiencies by year-end, and 21% faced material weaknesses. If weaknesses are found, companies may need to remediate controls, further driving up costs.

Breaking Down the Cost Impact

According to the 2023 SOX Compliance Survey:

- Average compliance cost per company: $1.5M - $2.2M per year

- SOX 404b audit fees alone: $500K - $1M annually

- Compliance hours increased by 58% due to external auditor demands

- Companies transitioning to 404b can see audit costs triple in the first year, as external auditors take zero chances, conducting deep-dive audits into financial controls, documentation gaps, and risk factors.

How Companies Can Reduce Costs?

Cutting SOX 404b compliance costs isn’t just about reducing expenses - it’s about optimizing processes. Here’s how companies can streamline compliance while lowering costs, with CloudEagle.ai helping at every step:

1. Automate Governance, Risk & Compliance (GRC) processes

Manual audits eat up time and resources, driving up costs. More than 60% of SOX compliance programs now use audit management and GRC platforms to reduce audit prep time and minimize human error.

With an automated GRC platform like CloudEagle.ai, you can:

- Automate access reviews - eliminating manual tracking of who has access to what

- Streamline SOX compliance reporting - generate reports in minutes, not days

- Reduce third-party risk - automate vendor access governance for audit-ready compliance.

Companies with >40% automated key controls are more likely to expand automation further, reducing audit complexity and lowering costs over time.

2. Conduct Internal Mock Audits

Waiting for an external auditor to flag control gaps can lead to costly remediation efforts. Proactively identifying weak controls and missing documentation can prevent last-minute surprises.

42% of companies have had to audit their vendors directly to ensure control effectiveness—highlighting the growing need for third-party access management.

With CloudEagle.ai, companies can:

- Automate mock audits to detect compliance gaps before an external audit

- Centralize vendor and app access data for easy reporting

- Reduce last-minute remediation costs by strengthening access governance

3. Strengthen Internal Controls Early

Companies with well-documented cost controls see higher auditor reliance - up to 34%, reducing redundant external testing and lowering compliance costs.

CloudEagle.ai helps:

- Ensure access control compliance by automating user provisioning and deprovisioning

- Maintain a secure audit trail track and log all access changes in real-time

- Reduce excessive auditor scrutiny by providing structured, audit-ready reports

4. Negotiate with Auditors to Reduce Over-Testing

Some external firms over-test, leading to unnecessary fees. Companies that mapped their internal controls to external SOC reports (68%) reduced audit redundancies, avoiding excessive testing and compliance costs.

Using CloudEagle.ai, companies can:

- Provide structured, real-time compliance reports to auditors upfront

- Reduce back-and-forth over missing documentation

- Minimize scope creep, ensuring audits stay cost-efficient

The takeaway?

SOX 404b is a compliance necessity, but it doesn’t have to drain your budget. With proactive planning, automation, and efficient controls, companies can cut costs while staying compliant.

Transitioning from SOX 404a to 404b

Companies navigating the shift in SOX 404a vs 404b must prepare for deeper scrutiny, increased documentation, and higher compliance costs. If your organization crosses the $75M public float threshold, SOX compliance shifts from management-led self-assessments (404a) to independent external audits (404b).

This transition isn’t just about meeting new regulatory requirements but also about preparing for deeper scrutiny, increased documentation, and higher compliance costs.

When Does A Company Move to SOX 404b?

A company moves from SOX 404a to 404b once it reaches Accelerated Filer status, which happens when:

- Public float exceeds $75M at the end of the second quarter.

- It has filed at least one annual report (10-K) with the SEC.

Companies that meet these criteria must prepare for their first external auditor attestation in the following year’s annual report.

What Changes in SOX 404b Compliance?

The biggest shift is external validation of internal controls. Unlike SOX 404a, where management assesses internal controls over financial reporting (ICFR), SOX 404b requires:

- Independent auditor attestation – External auditors must test, validate, and certify that ICFR is effective.

- Stronger documentation – Companies must provide detailed records proving that internal controls work as intended.

- More rigorous testing – Auditors conduct their control testing rather than relying solely on management’s assessment.

These changes mean higher compliance costs, increased internal effort, and a greater risk of deficiencies if controls aren’t strong enough.

How to Prepare for the 404b Transition?

To avoid audit headaches, companies should start preparing before they officially qualify as Accelerated Filers. Key steps include:

- Tightening internal controls early – Strengthen documentation and address control gaps before auditors find them.

- Standardizing risk assessments – Ensure risks are mapped to well-defined controls to avoid redundant testing.

- Improving audit readiness – Conduct internal mock audits to simulate the 404b review process.

- Streamlining financial reporting – Automate key compliance tasks to reduce manual errors and speed up audit prep.

Moving to SOX 404b isn’t optional, but a rushed transition can lead to costly deficiencies.

Companies that proactively strengthen internal controls, document processes, and plan for external audits early can reduce compliance stress and avoid unnecessary costs.

Common Pitfalls and Challenges in SOX 404 Compliance

SOX compliance isn’t just about meeting regulatory requirements - it’s about ensuring financial integrity while keeping costs under control.

Many companies underestimate the complexity of SOX 404 and fall into traps that lead to failed audits, higher expenses, and operational slowdowns.

Many companies assume that once they set up internal controls, they’re set for smooth audits. In reality, missteps in documentation, team coordination, and audit planning can disrupt operations, trigger deficiencies, and increase regulatory scrutiny.

Here are the biggest operational challenges companies face, and how to prevent them.

1. Underestimating the transition from 404a to 404b

Many companies assume the jump from management-led compliance SOX (404a) internal controls to 404 (b) external audits is minor. It’s not.

- External auditors dig deeper into control testing, documentation, and financial risk factors.

- Companies must provide verifiable evidence that their controls prevent financial misstatements.

- Gaps found during this transition often result in costly, last-minute remediation efforts.

→ How to avoid it: Don’t wait until you hit the $75M threshold. Start performing internal control testing like a 404b company before the transition. Conduct mock audits, strengthen control frameworks, and establish external audit expectations early.

2. Poor documentation and accountability gaps

If it’s not documented, it doesn’t exist - at least in the eyes of auditors. Lack of clear audit trails and ownership over financial controls can lead to compliance failures.

- Missing or inconsistent documentation leaves gaps auditors can’t verify.

- Unclear role ownership creates accountability issues in control execution.

- Manual record-keeping increases the risk of errors and audit delays.

→ How to avoid it: Ensure every internal control has clear documentation, assigned owners, and standardized reporting formats. Centralize financial reporting workflows so records remain consistent and easily accessible during audits.

3. Over-reliance on spreadsheets and manual processes

Many companies still track compliance efforts manually, leading to higher error rates, audit delays, and inefficiencies.

- Spreadsheets lack version control and create discrepancies in financial records.

- Manual workflows slow down audits, forcing teams to scramble for reports.

- Human error leads to inaccurate risk assessments and compliance deficiencies.

→ How to avoid it: Standardize compliance workflows and shift to structured reporting systems. Automating audit tracking, access reviews, and risk assessments ensures accuracy and consistency.

4. Poor coordination between teams

SOX compliance isn’t just a finance responsibility; it requires IT, procurement, operations, and legal teams. Yet, many companies treat it as an accounting issue, causing:

- Missed security risks due to a lack of IT-internal control alignment.

- Procurement missteps where vendor risks aren’t evaluated for compliance.

- Redundant efforts when different teams use separate compliance frameworks.

→ How to avoid it: Cross-functional alignment is critical. Establish a centralized compliance strategy, assign clear ownership across departments, and hold regular compliance review meetings.

5. Misalignment with external auditors

Companies often assume their internal control strategy will align with their auditors’ approach. But if audit scope and risk assessments aren’t clarified early, it can lead to:

- Surprise audit deficiencies when external auditors require more testing.

- Redundant control validations, leading to unnecessary work.

- Higher audit costs due to last-minute adjustments.

→ How to avoid it: Engage auditors early. Share your risk assessments and control framework before the audit begins. Ensure there’s alignment on testing expectations to prevent last-minute scope creep.

6. Treating SOX 404a vs 404b compliance as a one-time effort

Some companies treat SOX compliance as an annual checkbox exercise, only preparing controls right before the audit. The problem? Financial risks evolve, regulations tighten, and control failures compound over time.

- Static compliance strategies lead to outdated controls.

- Reactive fixes result in rushed remediations and audit stress.

- Regulatory changes can leave companies scrambling to adjust mid-year.

→ How to avoid it: Make SOX compliance a continuous process. Implement ongoing monitoring for internal controls, update risk frameworks regularly, and stay ahead of regulatory updates to avoid last-minute fire drills.

Best Practices to Reduce SOX 404 Compliance Costs

To reduce the significant costs associated with SOX 404 compliance while maintaining effectiveness, companies can adopt several best practices:

Centralize Information Management: Consolidate all compliance-related data and documentation into a single platform to eliminate redundant efforts and improve accuracy. This reduces time spent reconciling data from multiple sources and simplifies reporting.

Eliminate Manual Spreadsheets: Transition from spreadsheet-based processes to automated SOX compliance software. Automation reduces errors, accelerates data processing, and frees up staff for higher-value tasks.

Streamline Administrative Tasks: Use workflow automation and standardized procedures to cut down on routine administrative work. This allows compliance teams to focus on critical activities such as risk assessment and control testing.

Optimize and Rationalize Controls: Regularly review your SOX control framework to remove redundant or low-risk controls. Align controls closely with business objectives to focus efforts on areas that truly impact financial reporting integrity.

Leverage Technology and Automation: Implement robotic process automation (RPA), data analytics, and SOX compliance tools to speed up control testing and data collection. Automation can reduce compliance costs by improving efficiency and accuracy, enabling auditors to focus on exceptions and anomalies.

Outsource Select Compliance Activities: Consider partnering with specialized SOX compliance providers to gain expertise and technology advantages without heavy upfront investments. Outsourcing can be especially cost-effective for smaller or mid-sized companies lacking full in-house resources.

Plan a Phased, Strategic Approach: Develop a systematic, phase-by-phase compliance strategy to manage resources effectively and avoid last-minute rushes that drive up costs. Early planning helps mitigate surprises and spreads workload more evenly.

Maintain Continuous Documentation and Communication: Keep internal controls documentation up to date and maintain clear communication with auditors to reduce rework and delays during audits.

Staying SOX-Compliant Without the Headaches between 404a vs 404b

SOX 404 compliance is about passing audits but it’s more of a building financial transparency, reducing risk, and avoiding costly surprises.

Companies that take a proactive approach by strengthening internal controls, improving documentation, and aligning with external auditors early are the ones that navigate the transition in SOX 404a vs 404b to 404b with fewer disruptions and lower costs.

Staying ahead of SOX 404b requirements doesn’t have to be an uphill battle. CloudEagle.ai helps companies automate access controls, streamline audit reporting, and reduce compliance risks—all from one centralized platform. By eliminating manual processes and improving governance, CloudEagle.ai makes SOX compliance easier, faster, and more cost-effective.

FAQs

1. What is the SOX 404 policy?

SOX 404 requires publicly traded companies to establish, document, and maintain internal controls over financial reporting, and to annually assess and report on their effectiveness to reduce the risk of financial fraud.

2. What is the Sarbanes-Oxley 404 compliance test?

It is the process where management evaluates the design and operating effectiveness of internal controls over financial reporting, often followed by an external auditor’s attestation for applicable companies.

3. What is 404B compliance?

Section 404b compliance means an independent external auditor must attest to and report on management’s assessment of internal controls over financial reporting, adding an extra layer of assurance.

4. What is the public float for SOX 404b?

Companies with a public float of $75 million or more are generally subject to 404b auditor attestation. Smaller companies below this threshold, such as non-accelerated filers and smaller reporting companies, are typically exempt.

5. What is the difference between SOX 404 and 302?

SOX 404 focuses on management’s assessment and external auditor attestation of internal controls over financial reporting, while SOX 302 requires the CEO and CFO to personally certify the accuracy and completeness of quarterly and annual financial reports.

Read next:

- 7 Best Compliance Automation Tools

- Discover the 7 best compliance management tools to automate audits, ensure regulatory compliance, and simplify governance in 2024.

- Ensuring Compliance in SaaS Contracts: Legal and Regulatory Considerations

- Find out key legal and regulatory aspects for ensuring compliance in SaaS contracts. Handle complexities with these expert insights.

- SaaS Compliance: A Quick Guide for SaaS Buyers

- A concise guide for SaaS buyers, highlighting the importance of SaaS compliance while selecting SaaS applications.

.avif)

.avif)

.avif)

.png)